LOOK INSIDE!

Against All Odds

The Murray Koppelman Story

By Joshua M. Sklare

Published: 2013, 212 pages

Client: Murray Koppelman

Born: 1931, in Brooklyn, NY

Industry: Financial Services

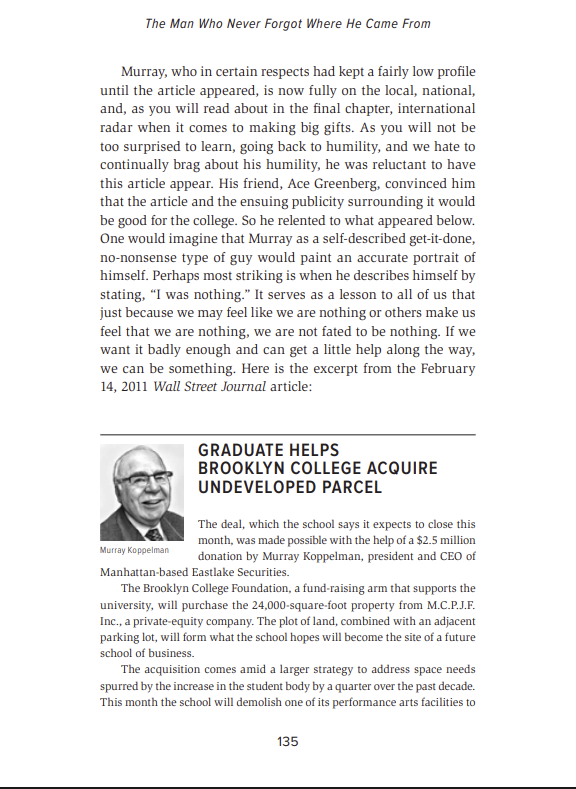

Immigrant parents of limited means raised Murray. His father worked in the garment industry, but lost his job in the Great Depression, and had to take public assistance to support his family for a time. Determined to break out of poverty, Murray started selling ice cream and frozen candy bars on Coney Island to help his family. After graduating from high school, he lived on a kibbutz in Israel for a year and a half, came back to America, served in the US Army overseas, and then got a degree in accounting from Brooklyn College. After serving as a CPA, he found his way to Wall Street, where he would eventually establish his own securities firm. A deeply committed philanthropist, the business school at Brooklyn College carries his name.